It was a very busy day in the financial markets, as investors digested a fresh batch of services PMI data, central bank commentary, and employment figures.

Fed Chair Powell’s remarks about economic resilience likely contributed to late-session volatility across asset classes while speculations about the upcoming OPEC+ meeting also pushed crude oil prices around.

Here are the economic updates and headlines you need to know:

Headlines:

- Jiji Press report suggested BOJ policymakers’ growing views against a premature rate increase unless there’s a big risk of consumer prices rising on factors such as a weaker JPY

- Australian economy grew slower than expected at 0.3% q/q in Q3 2024 (0.5% forecast)

- China Caixin services PMI declined to 51.5 in November (52.4 forecast) from 52.0

- Euro Area final services PMI revised higher to 49.5 from 49.2 in November:

- Spain services PMI for November: 53.1 (53.4 expected, 54.9 previous)

- Italy services PMI for November: 49.2 (50.9 expected, 52.4 previous)

- France final services PMI for November adjusted higher from 45.7 to 46.9

- Germany final services PMI for November adjusted lower from 49.4 to 49.3

- U.K. final services PMI for November upgraded to 50.8 from 50.0

- French government lost no-confidence vote, President Macron aims to name new Prime Minister swiftly

- U.S. ADP non-farm employment change in Nov: 146K (152K expected, previous revised down to 184K from 233K)

- U.S. ISM services PMI in Nov: 52.1 (55.7 forecast, 56.0 previous)

- Fed Chair Powell: “The economy is strong and it’s stronger than we thought it was going to be in September”

- BOE Governor Bailey signaled four interest rate cuts in 2025 if inflationary pressures continue cooling

- ECB head Lagarde reiterated their commitment to easing but expressed uncertainty about the pace

- EIA crude oil inventories fell 5.1M barrels vs. expected reduction of 1.6M (previous draw of 1.8M)

- Fed Beige Book: Economic activity saw slight uptick in November after stagnation period

- U.S. President-elect Trump nominated crypto-friendly Paul Atkins as SEC Chairperson

- OPEC+ might extend cuts to six months but cuts won’t be deeper – Reuters

Broad Market Price Action:

{kind=link}

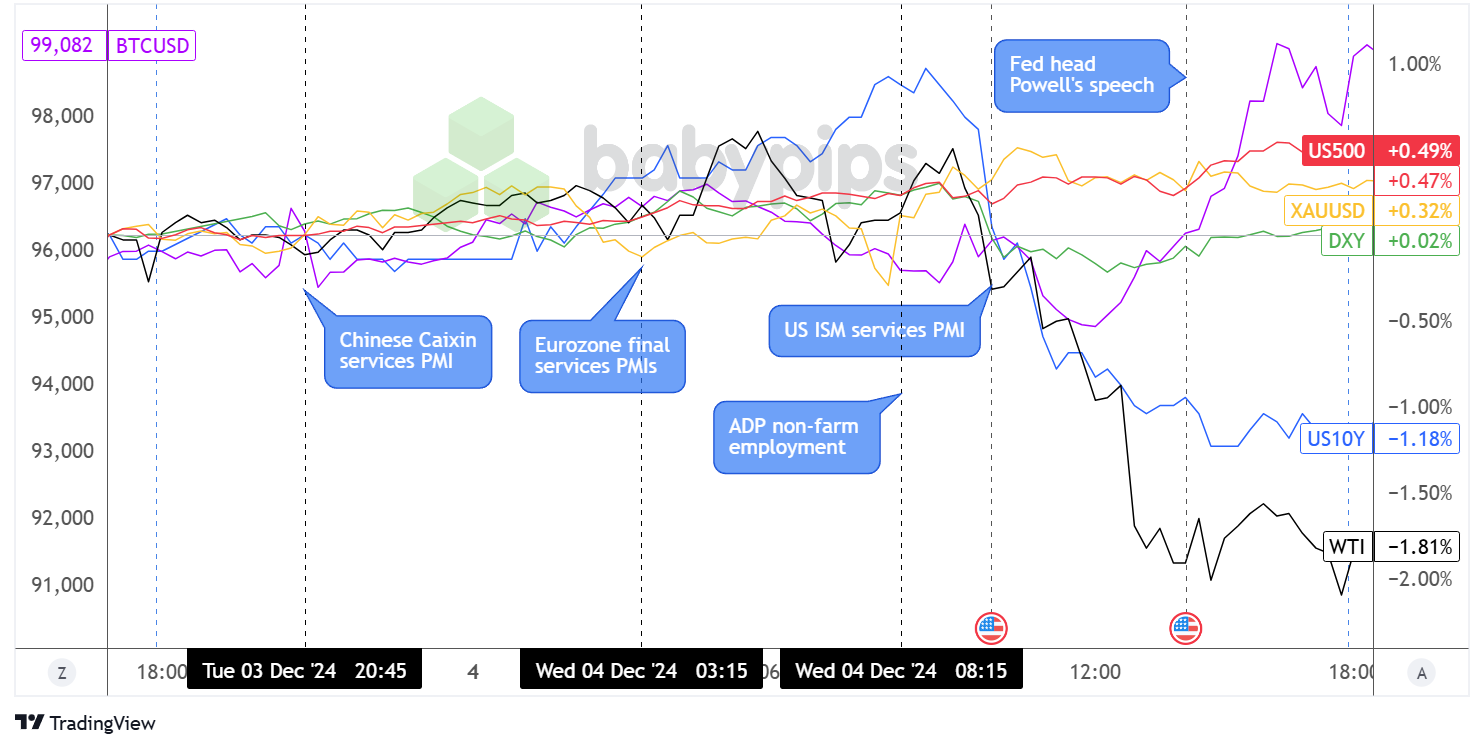

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Wednesday’s early Asian session saw pressure on risk assets following weaker-than-expected Chinese services PMI data, although most stayed within ranges while investors held out for top-tier data points.

U.S. Treasury yields cruised gradually higher leading up to the London session but eventually tumbled, with the 10-year yield dropping approximately 10 basis points intraday, possibly dragged by softer-than-expected ADP employment and ISM services data. Later on, Powell’s later comments about economic strength likely helped stem the decline.

On the other hand, U.S. equities demonstrated resilience, with all three major U.S. indices reaching record closing highs, supported particularly by technology sector strength following positive Salesforce earnings.

BTC/USD was on the back foot at the start of the U.S. session but soon staged a late-day rally approaching the $100K level, buoyed by Trump’s nomination of pro-crypto Paul Atkins as SEC Chairperson.

Crude oil struggled to hold its ground but eventually caved to bearish forces, as markets continued to price in expectations ahead of the OPEC+ meeting this week. WTI crude oil fell 1.81% despite a larger-than-expected drawdown in EIA inventories.

Meanwhile, gold maintained its upward momentum, closing 0.32% higher as traders balanced Powell’s hawkish tone against broader market uncertainties.

FX Market Behavior: U.S. Dollar vs. Majors:

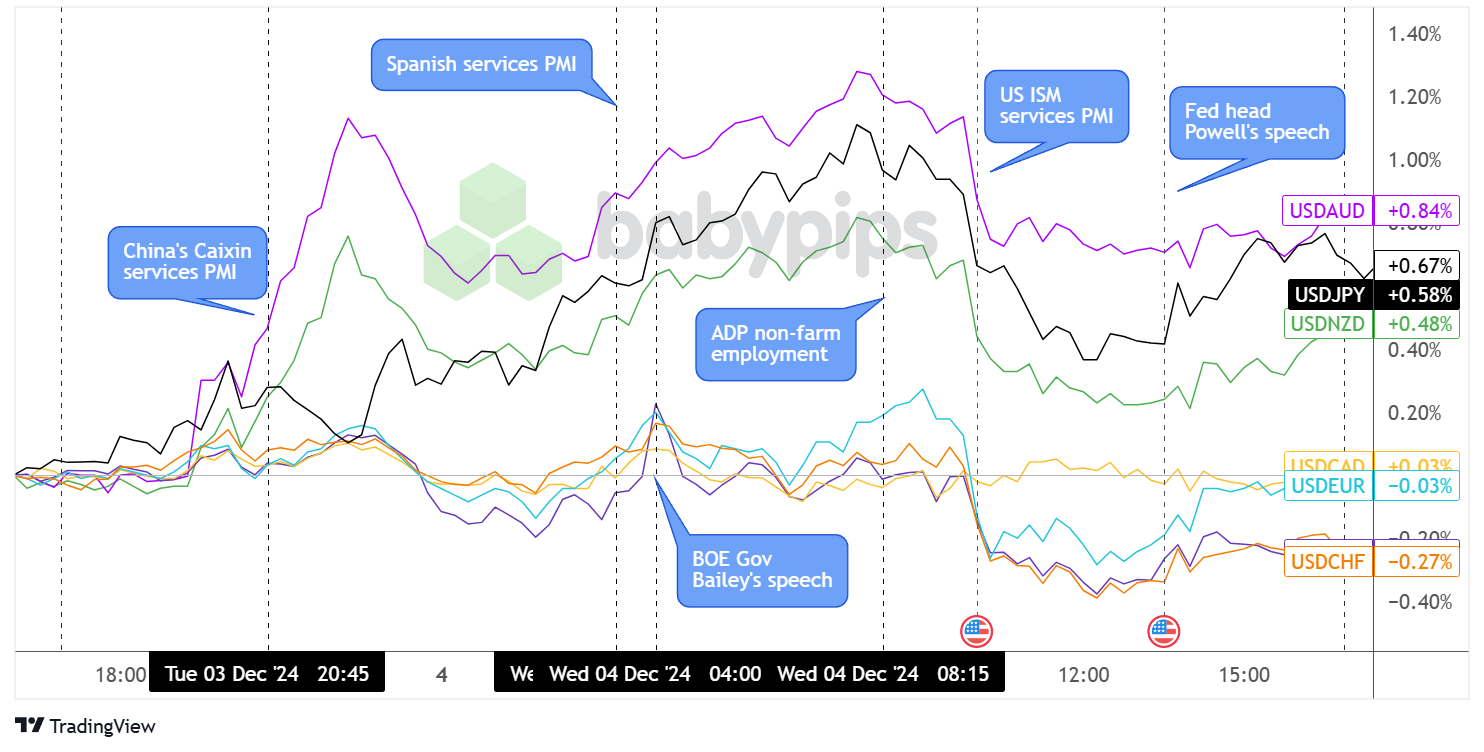

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar started the day on a positive note but was eventually pushed around by counter currency action and overall market sentiment.

Downbeat Australian GDP and weaker than expected Chinese Caixin PMI lifted the safe-haven U.S. currency versus the Aussie and Kiwi during the Asian session while USD/JPY also capped consecutive daily declines to trade higher until the start of the U.S. session.

GBP/USD dipped briefly lower on BOE Governor Bailey’s remarks about more interest rate cuts next year while EUR/USD barely sustained losses after the French government lost the no-confidence vote.

Initial weakness following soft ADP employment change data and a weaker ISM services PMI dragged the dollar south across the board, though these losses fizzled after Powell’s relatively hawkish remarks.

By the end of the trading day, the Greenback finished stronger against JPY, AUD, and NZD but weaker versus EUR and GBP.

Upcoming Potential Catalysts on the Economic Calendar:

- Swiss unemployment rate at 6:45 am GMT

- German factory orders at 7:00 am GMT

- U.K. construction PMI at 9:30 am GMT

- OPEC+ meetings going on

- U.S. Challenger job cuts at 12:30 pm GMT

- U.S. initial jobless claims at 1:30 pm GMT

- Canada’s Ivey PMI at 3:00 pm GMT

- BOE MPC member Greene’s speech at 5:00 pm GMT

Market volatility could remain elevated throughout the day, particularly for crude oil as the OPEC+ meetings are taking place.

Investors could also pay close attention to the U.S. Challenger job cuts report, which could contain some clues for Friday’s highly-anticipated NFP release, triggering strong reactions from the U.S. dollar along with the weekly initial jobless claims report.

Do keep an eye out for Canada’s Ivey PMI report since this could also shape expectations for the country’s upcoming jobs release.