Monday’s session was defined by the abrupt breakdown in US-Iran ceasefire negotiations, with President Trump publicly rejecting Tehran’s latest peace proposal and declaring the agreement on “massive life support.” Oil prices climbed in response to the diplomatic collapse while the S&P 500 managed another record closing high on chipmaker strength, illustrating a market environment in which geopolitical risk and equity resilience continued to coexist. China’s April inflation data delivered the session’s most significant macro surprise, with both CPI and PPI coming in above forecasts as the Iran war’s energy cost shock fed through visibly into the world’s largest manufacturing economy.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Australia Building Permits Final for March 2026: 9.0% y/y (9.0% y/y forecast; 14.0% y/y previous)

- Australia Private House Approvals Final for March 2026: 0.9% m/m (0.9% m/m forecast; 0.2% m/m previous)

-

China CPI Growth Rate for April 2026: 1.2% y/y (0.9% y/y forecast; 1.0% y/y previous)

- China PPI Growth Rate for April 2026: 2.8% y/y (1.7% y/y forecast; 0.5% y/y previous)

- U.S. Existing Home Sales for April 2026: 0.2% m/m (2.1% m/m forecast; -3.6% m/m previous)

- Bank of Canada Market Participants Survey: the Bank of Canada reported that financial market participants expect moderate economic growth (median 1.6% GDP by end-2026), a persistent negative output gap, and headline inflation easing to 2.6% by year-end before returning to the 2% target. Geopolitical risks are now viewed as the top downside concern, while participants anticipate the BoC policy rate will remain at 2.25% through December 2026, with the first hike expected in March 2027.

- On Monday, U.S. President Trump said the ceasefire between the US and Iran was on “massive life support” after his rejection of Tehran’s latest peace offer.

Promoted: Day traders & Scalpers have better odds of making great decisions if they see market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Monday’s session unfolded in two broadly distinct phases for most assets. A risk-cautious tone prevailed through the overnight and early European hours as markets absorbed the renewed US-Iran ceasefire deterioration, before a more decisive directional leg emerged in the New York session as Trump’s Oval Office remarks around 1:15 pm ET made clear that any near-term diplomatic resolution remained unlikely.

WTI crude oil was the session’s most prominent mover and the clearest expression of the geopolitical backdrop. The session traced a wide intraday path: oil surged through the Asia session as Trump rejected Iran’s proposals and reports circulated that Israel viewed removal of Iranian nuclear material as an active war priority, pushing the contract toward session highs near $96.85 before retreating sharply through the London hours to lows around $93.29. A recovery through the US afternoon followed as Trump’s public comments hardened the diplomatic deadlock, with Saudi Aramco’s CEO noting that even an immediate reopening of the Strait of Hormuz would take months before normal market conditions could be restored.

Gold closed near $4,737, up approximately 1.06% on the session. Gold declined steadily through the Asian and London sessions, falling from roughly $4,715 toward lows near $4,648 before staging a sharp recovery shortly after the New York open. The metal rallied from approximately $4,680 to a session high near $4,748 before settling around $4,737. With no direct gold-specific catalyst apparent for the US session reversal, the move may have reflected a combination of the renewed geopolitical risk premium from Trump’s deteriorating Iran remarks and broader safe-haven positioning ahead of Tuesday’s US CPI release.

The S&P 500 closed at 7,412.8, up 0.23% on the session, confirming another record closing high supported primarily by strength in chipmakers. The index traded in a narrow sideways range through the overnight and European sessions before a sharp surge near the US equity open pushed the index above 7,395 and toward session highs near 7,428 before modest late-session profit-taking trimmed gains into the close.

U.S. 10-year Treasury yields closed at approximately 4.4%, up 1.33% on the session. Yields ground steadily higher through the US afternoon, consistent with the oil-driven inflation risk narrative that gained traction as the session progressed. Wall Street firms including Goldman Sachs and Bank of America pushed back their rate cut forecasts, with Pimco suggesting the Iran oil shock has put cuts off the table and hikes back on the agenda. Tuesday’s April CPI report is widely expected to reinforce that narrative.

Bitcoin closed at $81,989.2, up 2.32% on the session. Bitcoin sold off through much of the Asian and London sessions, declining from early highs near $82,450 to lows around $80,430, before recovering steadily through the US hours. With no direct Bitcoin-specific catalysts apparent during the session, the recovery may have reflected broader stabilization in risk appetite as equities logged gains.

Promotion: If your confidence has grown in your market awareness & strategies with this market recap, and you wanna take action, Maven Trading can help. They provide simulated funding challenges starting as low as $13, allowing you to trade major pairs with professional-sized capital. No time limits mean you can take swing plays on these market themes without the pressure of a ticking clock.

Learn More About Maven Trading Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

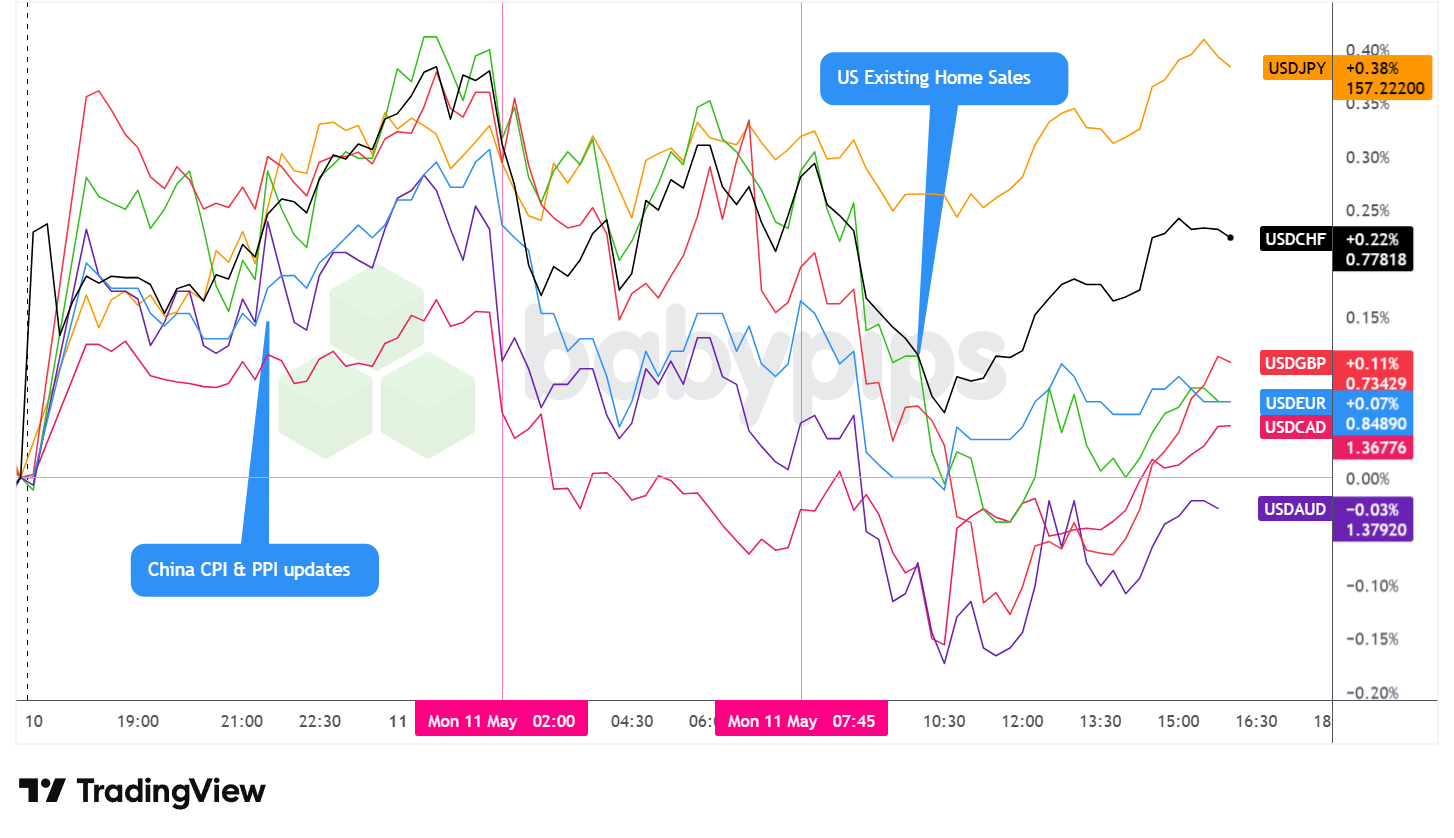

The U.S. dollar traded with a clear three-phase profile on Monday, ultimately closing in mixed but arguably net positive territory against major currencies on a daily basis.

During the Asian session, the dollar spiked sharply higher against the majors just after the open and then stabilized before drifting higher through the remainder of the session. The move likely reflected the reopening risk premium from the weekend’s US-Iran headlines: Trump’s rejection of Iran’s proposal and Tehran’s sweeping counter-framework, which demanded Hormuz sovereignty, sanctions relief, war compensation, and an end to the U.S. naval blockade before nuclear discussions could even begin, left little prospect for near-term resolution.

That backdrop may have supported some capital flow into the dollar. The yuan outperformed peers on the session, supported by China’s stronger-than-expected April CPI and PPI prints. The PBOC set the USD/CNY reference rate at 6.84, notably above the estimated 6.79, signaling some tolerance for modest yuan weakness alongside the broader dollar bid.

During the London session, the dollar traded net lower against the major currencies from the open through approximately one hour after the US equity market open around 10:30 am ET. The reversal from Asian session highs was broad-based, with most USD pairs declining in a coordinated fashion that suggested a general pullback from the overnight risk-premium bid rather than a currency-specific driver. ECB commentary from de Guindos and Kocher struck cautious tones, and BoE’s Greene also signaled patience on rate decisions, providing limited directional catalyst for European currencies on a fundamental basis.

During the U.S. session, the dollar gradually recovered from its London session lows and drifted higher through the remainder of the day. Trump’s Oval Office remarks around 1:15 pm ET, in which he called the ceasefire on “massive life support” and Iran’s proposal a “piece of garbage,” reinforced the ongoing geopolitical risk premium that had underpinned the Asia session’s dollar strength. U.S. Existing Home Sales for April came in significantly below forecast at 0.2% month-on-month versus 2.1% expected, though the miss appeared to generate limited lasting impact on dollar direction.

Promotion: When the Market Swings, Are You Reacting or Executing?

In “Positive Trading Psychology,” renowned psychologist Brett Steenbarger reveals in his newest book that the secret to navigating volatility isn’t “fixing” your flaws—it’s doubling down on your innate character strengths. Learn how to stay clinical while the rest of the market is emotional, turning sudden market shaking news into your professional edge.

Learn more about “Positive Trading Psychology: Turning personal strengths into trading strengths” on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- U.K. BRC Retail Sales Monitor for April 2026 at 11:01 pm GMT

- Japan Household Spending for March 2026 at 11:30 pm GMT

- BoJ Summary of Opinions at 11:50 pm GMT

- Australia Westpac Consumer Confidence Change for May 2026 at 12:30 am GMT

- Australia NAB Business Confidence for April 2026 at 1:30 am GMT

- Japan Leading Economic Index Prel for March 2026 at 5:00 am GMT

- Germany Inflation Rate Final for April 2026 at 6:00 am GMT

- Swiss Producer & Import Prices for April 2026 at 6:30 am GMT

- U.S. Fed Williams Speech at 7:15 am GMT

- Germany ZEW Economic Sentiment Index for May 2026 at 9:00 am GMT

- Euro area ZEW Economic Sentiment Index for May 2026 at 9:00 am GMT

- U.S. NFIB Business Optimism Index for April 2026 at 10:00 am GMT

- U.S. ADP Employment Change Weekly for April 25, 2026 at 12:15 pm GMT

- U.S. CPI Growth Rate for April 2026 at 12:30 pm GMT

- U.S. Fed Goolsbee Speech at 5:00 pm GMT

- U.K. BoE Woods Speech at 5:30 pm GMT

- U.S. Monthly Budget Statement for April 2026 at 6:00 pm GMT

Tuesday’s calendar is headlined by the U.S. April inflation report at 12:30 pm GMT, which carries the session’s highest event risk given the Iran war’s ongoing energy cost transmission and the broad repricing of Fed rate expectations on Wall Street. Economist consensus points to a 0.6% monthly gain, which would follow March’s largest monthly advance since 2022. A print in line with or above expectations would likely reinforce the case for the Fed to hold steady into year-end and could push Treasury yields and the dollar higher, while a downside surprise may spark a short-lived repricing of easing expectations.

The BoJ Summary of Opinions will also be worth monitoring for any shift in tone following recent yen weakness, particularly with USD/JPY back above 157.00. Germany’s final April inflation reading and the ZEW economic sentiment indices for Germany and the euro area round out the European session calendar, while Fed Williams speaks ahead of the US open and Goolsbee follows after the CPI release, both of which could add color to how policymakers are weighing the inflation outlook against the geopolitical backdrop.

Stay frosty out there, forex friends!

Monday’s market was shaped by the breakdown in US-Iran ceasefire negotiations, driving oil prices and triggering safe-haven flows across currencies and assets. If you’re wondering how geopolitical shocks like this actually move the forex market, Premium members can read our lesson:

📖 Geopolitical Risk, Trade Policy, and Safe Haven Flows

Reading this helps you understand which currencies typically gain from geopolitical risk premiums, how safe-haven flows reshape dollar pairs, and what patterns to watch when headlines move markets instead of economic data.

And if you’re not a Premium subscriber yet, consider joining.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what the market’s doing in the moment, but the fundamental forces behind the move