Hotter-than-expected U.S. inflation data drove Treasury yields sharply higher and pushed equities lower on Tuesday, while crude oil surged as the U.S.-Iran conflict showed no signs of resolution. The April consumer price index topped forecasts across both headline and core measures, reinforcing expectations that the Federal Reserve will keep rates on hold and fueling market bets on a potential hike in 2027.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Japan Household Spending for March 2026: -1.3% m/m (1.1% m/m forecast; 1.5% m/m previous)

- Australia NAB Business Confidence for April 2026: -24.0 (-32.0 forecast; -29.0 previous)

- Japan Leading Economic Index Prel for March 2026: 114.5 (109.0 forecast; 113.3 previous)

- Germany Inflation Rate Final for April 2026: 2.9% y/y (2.9% y/y forecast; 2.7% y/y previous)

- Swiss Producer & Import Prices for April 2026: -2.0% y/y (-2.6% y/y forecast; -2.7% y/y previous)

- Germany ZEW Economic Sentiment Index for May 2026: -10.2 (-21.0 forecast; -17.2 previous)

- Euro area ZEW Economic Sentiment Index for May 2026: -9.1 (-23.0 forecast; -20.4 previous)

- U.S. NFIB Business Optimism Index for April 2026: 95.9 (96.2 forecast; 95.8 previous)

- U.S. ADP Employment Change Weekly for April 25, 2026: 33.0k (39.25k previous)

-

U.S. CPI Growth Rate for April 2026: 3.8% y/y (3.6% y/y forecast; 3.3% y/y previous)

- U.S. Core Inflation Rate for April 2026: 2.8% y/y (2.6% y/y forecast; 2.6% y/y previous)

Promoted: Day traders & Scalpers have better odds of making great decisions if they see market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

{kind=link}

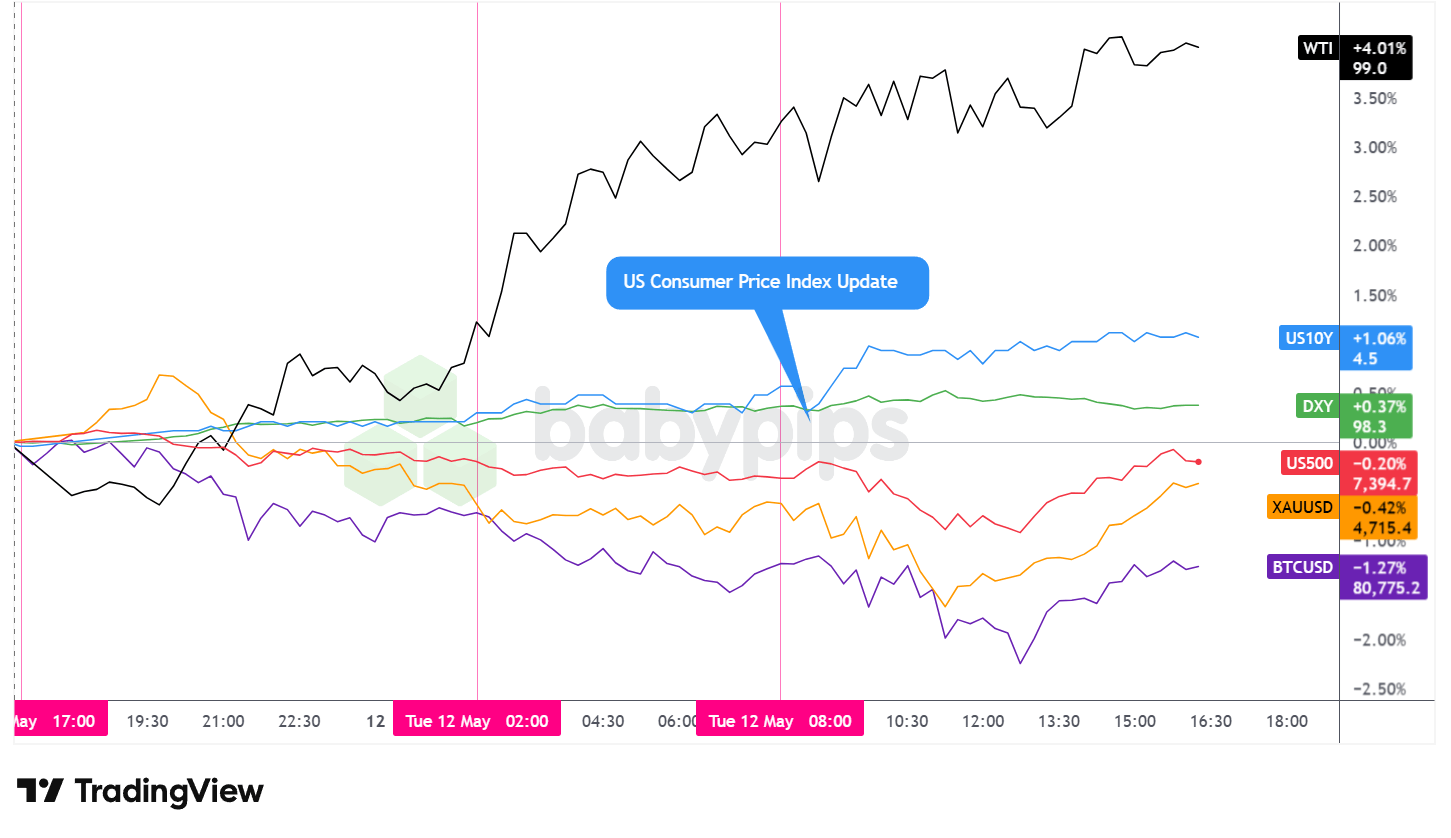

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

WTI crude oil led Tuesday’s broad market session, climbing 4.01% to trade near $99.0 per barrel. The rally built steadily from the Asian open and extended throughout the day as U.S.-Iran conflict headlines showed no sign of improvement. President Trump described the ceasefire as on “life support,” and CNN reported he is now more seriously weighing a return to major combat operations, frustrated by the continued closure of the Strait of Hormuz and the lack of meaningful progress in nuclear negotiations. On the intraday chart, WTI climbed continuously from the Asia open, adding more than four dollars per barrel before briefly approaching the $99.30 area and consolidating near session highs.

The 10-year Treasury yield rose 1.06% on the day to approximately 4.5%, with the move accelerating sharply after the April CPI release. Headline inflation came in at 3.8% year-on-year, the highest reading since 2023, topping the 3.6% forecast and up from 3.3% in March. The monthly reading of 0.6% also exceeded the 0.5% expected. Core CPI, which excludes food and energy, rose 2.8% year-on-year and 0.4% month-on-month, both above the 2.6% and 0.3% respective forecasts. After accounting for rising prices, wages declined in April from a year earlier, the first such drop since 2023, with gasoline prices up sharply since the conflict began and grocery prices posting their largest monthly jump since 2022.

The S&P 500 declined 0.20% to close near 7,394.7, pulling back from record territory. The selloff was concentrated in semiconductor stocks, with a gauge of chipmakers falling roughly 3% and the Nasdaq 100 sliding nearly 1%, as analysts noted the sector’s nearly 70% surge over the prior six weeks had left valuations stretched heading into a catalyst that pointed the wrong way on inflation. The index dipped to approximately 7,338 in the early U.S. session before recovering through the afternoon. Market commentary cited the combination of a still-resilient labor market and the diminished prospect of Federal Reserve rate relief as complicating the near-term outlook for high-valuation growth equities. One market participant quoted by Bloomberg noted that the rise in core CPI suggests elevated energy prices are making themselves felt across the broader economy, and that new Fed leadership is unlikely to produce an immediate dovish shift.

Gold declined 0.42% to trade near $4,715.4. The precious metal’s intraday chart showed a spike to approximately $4,774 shortly after the Sunday close, followed by a gradual and largely uninterrupted selloff through the Asian and London sessions. The metal dipped to approximately $4,639 in the wake of the CPI data before recovering through the U.S. afternoon. The day’s net decline may appear counterintuitive given the concurrent surge in crude oil and elevated geopolitical risk, though the sharp rise in Treasury yields and the firmer dollar likely weighed on the non-yielding asset.

Bitcoin declined 1.27% to trade near $80,775.2. The cryptocurrency sold off steadily through the Asian and London sessions, reaching a low near $79,809 following the CPI release before staging a partial recovery through the U.S. afternoon. No direct crypto-specific catalysts were apparent; the weakness possibly reflected broader risk-off positioning in the wake of the inflation data.

Promotion: If your confidence has grown in your market awareness & strategies with this market recap, and you wanna take action, Maven Trading can help. They provide simulated funding challenges starting as low as $15, allowing you to trade major pairs with professional-sized capital. No time limits mean you can take swing plays on these market themes without the pressure of a ticking clock.

Learn More About Maven Trading Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

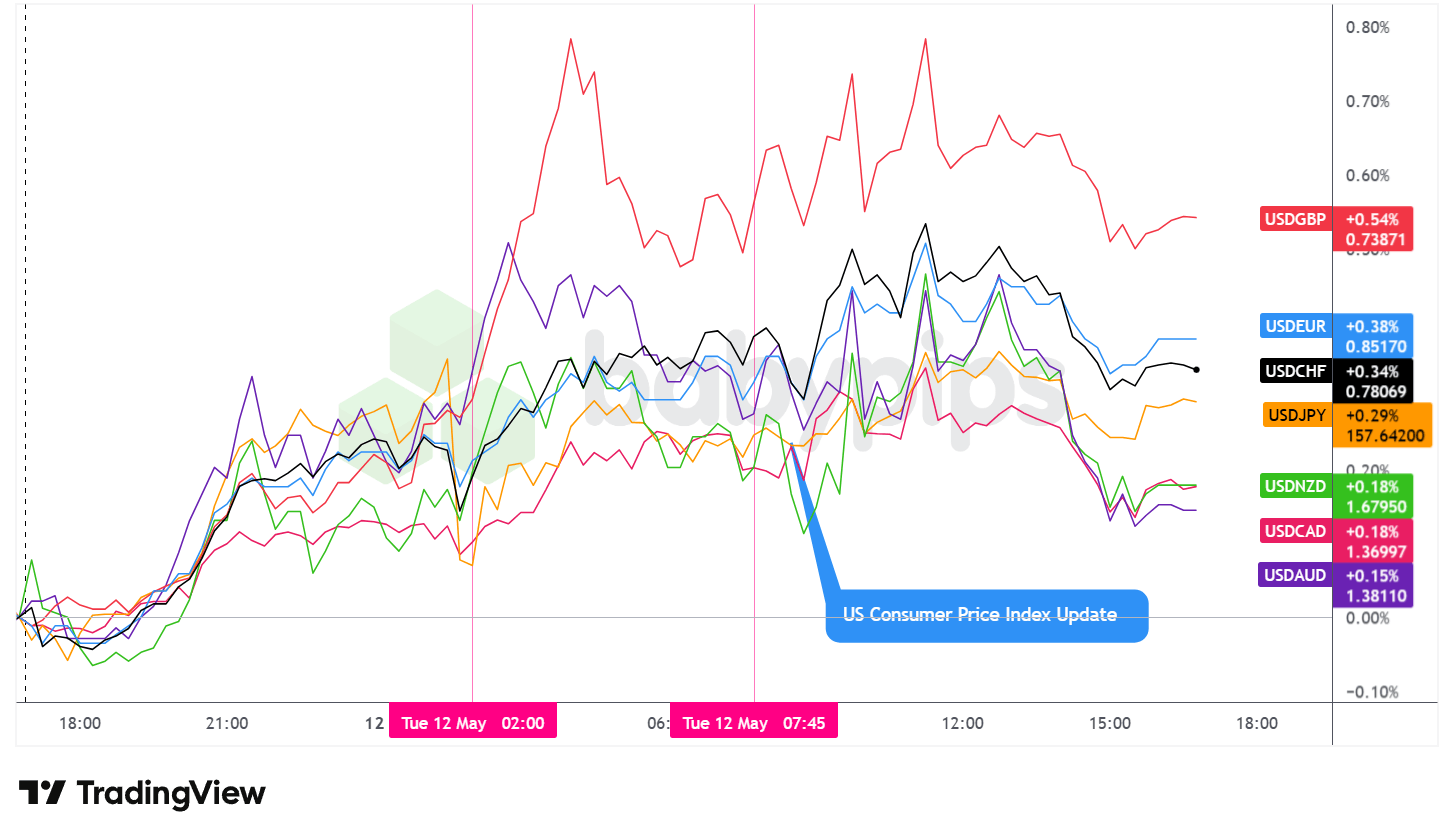

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar traded net higher against all major currencies on Tuesday, emerging as the session’s best-performing major. The greenback’s gains were heavily front-loaded, with notably strong upside momentum through the Asian session, while the U.S. session saw a partial pullback that still left the dollar firmly ahead at the close.

During the Asian session, the dollar gained ground broadly, with the advance likely supported by safe-haven positioning as U.S.-Iran conflict headlines deteriorated overnight. Reports indicated Trump’s national security team met at the White House to review military options, though a major decision was not expected before the president’s departure for Beijing.

The Bank of Japan’s Summary of Opinions, published Tuesday, struck a notably hawkish tone, with board members warning that upside inflation risks are growing as crude oil prices surge and several members flagging possible rate hikes as early as the next meeting. Despite this, the yen remained under broad selling pressure, with the macro backdrop widely seen as negative for the Japanese currency.

A sharp and short-lived whipsaw in USDJPY during the Asian session has been attributed to a suspected intervention, though the move was quickly reversed and the pair rallied back toward the 158.00 resistance area. Finance Minister Katayama confirmed that Japan and the U.S. reaffirmed close coordination on currency markets, including on intervention, following her meeting with Treasury Secretary Bessent in Tokyo. Bessent also posted on X, describing the level of communication between both sides in addressing “undesirable, excess volatility” in currency markets as “constant and robust.” Despite the reaffirmation, the dollar held its gains against the yen through the Asian and London sessions, possibly suggesting market participants interpreted the coordination language as a tactical signal rather than a commitment to sustained yen strength.

During the London session, the dollar continued to trade with a net bullish lean ahead of the U.S. CPI print. The most notable intraday FX development was the USDJPY whipsaw linked to the suspected intervention noted above, which generated a brief spike in the yen before reversing.

In terms of regional economic data, the Germany and Euro area ZEW Economic Sentiment readings for May both came in significantly better than forecast, with the German index printing at -10.2 against a -21.0 expectation and the Euro area reading at -9.1 against a -23.0 forecast. While both readings remained in negative territory, the magnitude of the beats was notable. However, with conditions still worsening and the broader European outlook clouded by energy costs tied to the Iran conflict, the data appeared to generate limited FX reaction. The NFIB Small Business Optimism Index for April was essentially unchanged at 95.9, with inflationary pressures continuing to rank as the primary concern among small business owners.

The U.S. session opened with the April CPI report delivering a clear upside surprise. Headline inflation accelerated to 3.8% year-on-year and 0.6% month-on-month, while core CPI came in at 2.8% year-on-year and 0.4% month-on-month, all above their respective forecasts.

The data reinforced expectations that the Federal Reserve will hold rates at current levels for an extended period, with market pricing shifting to reflect a greater probability of a hike in 2027. Following the release, the dollar experienced some choppiness before pulling back gradually through the afternoon. Despite the U.S. session retreat, the greenback closed the day as the top-performing major currency, with gains registered across all pairs on the overlay chart.

Promotion: When the Market Swings, Are You Reacting or Executing?

In “Positive Trading Psychology,” renowned psychologist Brett Steenbarger reveals in his newest book that the secret to navigating volatility isn’t “fixing” your flaws—it’s doubling down on your innate character strengths. Learn how to stay clinical while the rest of the market is emotional, turning sudden market shaking news into your professional edge.

Learn more about “Positive Trading Psychology: Turning personal strengths into trading strengths” on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- Japan Current Account for March 2026 at 11:50 pm GMT

- Japan Bank Lending for April 2026 at 11:50 pm GMT

- Australia Westpac Consumer Confidence Change for May 2026 at 1:30 am GMT

- Australia Wage Price Index for March 31, 2026 at 1:30 am GMT

- Australia Home Loans for March 31, 2026 at 1:30 am GMT

- New Zealand Business Inflation Expectations for June 30, 2026 at 3:00 am GMT

- Japan Eco Watchers Survey Outlook for April 2026 at 5:00 am GMT

- Germany Wholesale Prices for April 2026 at 6:00 am GMT

- France Inflation Rate Final for April 2026 at 6:45 am GMT

- Euro area Employment Change Prel for March 31, 2026 at 9:00 am GMT

- Euro area GDP Growth Rate 2nd Est for March 31, 2026 at 9:00 am GMT

- U.S. MBA 30-Year Mortgage Rate for May 8, 2026 at 11:00 am GMT

- U.S. MBA Mortgage Applications for May 8, 2026 at 11:00 am GMT

- U.S. PPI for April 2026 at 12:30 pm GMT

- Germany Current Account for March 2026 at 12:45 pm GMT

- U.K. BoE L Mann Speech at 2:00 pm GMT

- U.S. EIA Crude Oil Stocks Change for May 8, 2026 at 2:30 pm GMT

- U.S. Fed Collins Speech at 3:30 pm GMT

- U.S. Fed Kashkari Speech at 5:15 pm GMT

- BoC Summary of Deliberations at 5:30 pm GMT

- Euro area ECB Lane Speech at 7:00 pm GMT

- Euro area ECB President Lagarde Speech at 7:15 pm GMT

The most significant event on the near-term horizon is President Trump’s state visit to China from May 13 to 15, which marks the first visit to Beijing by an American president in nearly nine years. Trump told reporters Tuesday that trade will be the primary focus of the summit, with both sides expected to discuss an extension of the trade truce reached last fall, possible Chinese purchases of U.S. agricultural goods and other products, and the framework for a bilateral board of trade. He downplayed the likelihood of the Iran conflict featuring heavily, though Beijing has been signaling it may be positioning itself as a potential broker on the Strait of Hormuz, and any concrete cooperation on reopening the waterway could deliver an immediate shock to energy markets in either direction.

For traders, the summit readout is likely to move currencies, commodities, and equities in real time. A constructive outcome that extends the trade truce and signals Strait cooperation could lift risk appetite broadly, put pressure on the dollar, and support Asian equities and the yuan. A breakdown or combative joint statement, on the other hand, could trigger a flight to safety, with the dollar and gold as the likely beneficiaries and tech stocks under additional pressure. A polite but inconclusive summit, which many analysts consider the most probable scenario, may generate an initial muted reaction before markets refocus on the underlying unresolved tensions. USD/CNY, the Nasdaq 100, and agricultural futures have been identified as the clearest real-time signals for how markets are reading the summit outcome.

On the data side, U.S. April PPI at 12:30 pm GMT Wednesday will be closely watched following Tuesday’s above-forecast CPI. A second consecutive upside inflation surprise could further cement expectations of a prolonged Federal Reserve hold and reinforce the shift in market pricing toward a possible 2027 hike.

Multiple Fed speakers are scheduled throughout the day, with Collins at 3:30 pm GMT and Kashkari at 5:15 pm GMT likely to draw attention given the fresh inflation data. The BoC Summary of Deliberations at 5:30 pm GMT may shed light on how Canadian policymakers are weighing energy-driven inflation against domestic growth conditions.

In the evening, ECB President Lagarde at 7:15 pm GMT will be monitored for any updated commentary on the European growth and inflation outlook. Overnight, Australia’s Wage Price Index at 1:30 am GMT will be relevant for RBA rate expectations, with domestic business conditions having fallen to their second-lowest reading since 2020.

Stay frosty out there, forex friends!

Tuesday’s inflation data surprised to the upside, moving Treasury yields and currency prices sharply, but understanding why economic releases create such immediate and dramatic price reactions is something most traders never learn. Premium members can read our lesson:

📖 From Data to Price Action: What Happens When Big News Hits

Reading this helps you understand what actually happens in the FX market the moment major economic data lands, the difference between the initial algorithmic spike and the secondary analytical move, and the common traps that catch unprepared traders.

And if you’re not a Premium subscriber yet, now’s a good time to sign up with a limited time 35% discount!

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what the data number was, but how the market actually processes that surprise and where the real trading opportunity emerges after the initial spike.